What is a long put spread? A long put spread is a bearish options strategy that is often launched when the trader feels the underlying stock is likely to decrease but has a possible downside target in mind at the same time. This is because a long put spread allows the trader to profit from a decline in the underlying stock's price. The two-tiered trade is an option to just purchasing a put, which lowers the initial cost of entry and the investor's maximum risk on the transaction. However, the profit potential offered by a bear put spread is smaller than that offered by a long put position.

Entering a Long Put Spread

Let's say the current price of Stock XYZ is $68 a share, and our hypothetical trader anticipates a decline in the stock price. However, the XYZ options are priced with quite high expectations for the market's volatility, indicating that the contracts are currently fairly rich. In addition, the price of XYZ shares may find support at $65 in the near future.

The trader determines that opening a long put spread is better than merely purchasing the May 67.50 put option. She invests $0.40 to buy a put with a strike price of 67.50 and concurrently invests $0.10 to open a put with a strike price of 65. When the premium received for purchasing the long put is subtracted from premium received for selling the short put, the result is a net negative of $0.30 for the transaction. When multiplied by the number of shares required for one contract, the total cost of entry for the trader is $30.

Measuring Potential Gains and Losses

If XYZ falls below $67.20 (the strike price of the acquired put less the net debit), then the spread will begin to generate a profit before the May options expiry. The most favorable outcome would be for XYZ to close at precisely $65 upon the contract's expiry. Because of this, our trader will be able to collect the maximum return on the long put, which is equal to the difference between the two options strikes, less the net debt, which comes to ([67.50 - 65] - $0.30 = $2.20) $220. Meanwhile, the short put with a strike price of 65 will be allowed to expire without any value.

On the other side, trader will incur loss if a price of Stock XYZ expires at or above $67.50 throughout the contract. In this scenario, the trader will be required to give up the original net debit of $30, which is the maximum amount that may be lost on the play.

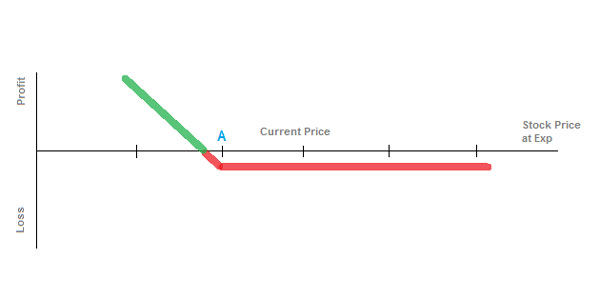

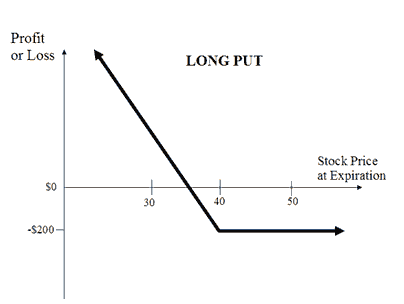

How to Set Up a Long Put

When investors acquire a put option contract, they take the first step in initiating a long put strategy. Put options are displayed in an option chain, which provides pertinent data for each possible strike price and expiry date, as well as the bid-ask price. The fee that must be paid to participate in the transaction is known as the premium. When determining the value of an option's premium, players in the market consider several criteria. These considerations include the strike price of the stock price, the amount of time remaining before expiry, and volatility.

In general, put options cost more than call options for the same underlying asset. This price skew exists because investors are ready to pay a larger premium to hedge their holdings and protect themselves from potential losses.

What's the Difference?

As was discussed before, a trader might minimize the total risk of the bearish trade and get closer to breakeven by entering into a long put spread rather than purchasing a put option. On the other hand, the potential for a reduced payoff when compared to a conventional put move is a trade-off.

For illustration purposes, let's imagine that the price of Stock XYZ suddenly increased to $70 just before the options expired. In this scenario, the spread strategy has incurred a loss of just $30, whereas the trader who only purchased the May 67.50 put is looking at a potential loss of $40 ($0.40 multiplied by 100 shares for each contract).

Or, let's assume XYZ drops to $67.15. The spread strategy is currently in the black in this case because the shares are now trading for less than breakeven at $67.20. For the one buyer of puts into making a profit, XYZ would need to drop even further, below $67.10 (the strike price less the premium paid), before the trade would be considered profitable.

Nevertheless, suppose that the price of Stock XYZ falls to $50 before the options for May expire. Because the short 65-strike put was used, the spread strategy will still pocket just $2.20, equivalent to $220. On the other hand, the solitary put buyer will have an option with $15, or $1,500, merely in terms of its intrinsic worth.