Introduction

Title loans for vehicles are commonly used to illustrate the subprime loan market. The borrowers typically have low incomes or poor credit, making it difficult to qualify for alternative financing like a personal line of credit, which is why these loans are so popular (LOC). Loans secured by a car tend to have high-interest rates due to the greater risk of default. Critics of car title loans say they are a form of predatory lending because they prey on desperate borrowers with few other options. The use of non-annualized interest rates is one contentious aspect of car title loans and short-term loans more generally.

How Do Car Title Loans Work?

Title loans on automobiles are notorious for their prohibitive interest rates. A title loan's monthly finance charge of 25% could result in an annual percentage rate (APR) of 300% in addition to any other fees. A borrower of a $1,000 car title loan can expect to pay around $1,200. Moreover, the average borrower must devote roughly half their monthly gross income to paying back the auto title loan. Some states allow you to renew or roll over a car title loan into a new one if you cannot pay it off by the end of the initial 15 or 30-day term. Though this option could help you keep your car, it will also increase your interest payments. The total amount owed (principal plus interest) may be due all at once at the end of the term, or it may be broken up into installments.

Alternatives to Car Title Loans

If your credit is less than stellar, you might feel trapped. Given this, it's no surprise that title loans remain popular despite their risks to borrowers' financial security. Avoiding this type of loan is still recommended. These alternate options to title loans can provide borrowers with poor credit access to funds.

Family and Friends

Asking for financial help from loved ones can be awkward. You should only apply for an informal loan if you know you can repay the money.

Bad Credit Personal Loan

Fortunately, private loan companies are willing to work with borrowers with low credit scores. You may pay more in interest and fees than someone with good or excellent credit, but you will likely pay much less than a title lender, and the repayment period will be much more generous.

Financial Assistance Services

A person's eligibility for short-term cash aid from their state or local government depends on where they live. Through these programs, financial aid is available for medical costs, food, child care, utility bills, transportation, and more.

Payroll Advance

Your company may give you a paycheck in advance. This may cause issues if and when you need those funds, but it will give you time to figure things out.

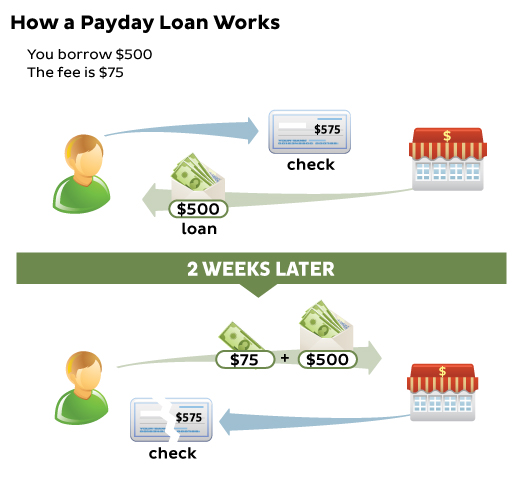

Payday Alternative Loan

Some credit unions provide members with an alternative to payday loans. Since the APR on these loans cannot go above 28%, they are significantly more affordable than some more conventional personal loans.

Credit Counseling

Working with a credit counselor can be helpful if you have money problems due to excessive debt. Credit counseling services may be able to help you lower your interest rates and waive late fees on your existing loans through a debt management program.

Conclusion

Loans against the value of a vehicle can be a quick and easy way to get money. But the risks aren't worth the costs, and you might end up in a worse position after taking out the loan. If you've looked at every other option and still need money, a car title loan might be your last resort; make sure to read the fine print. Federal law mandates that title lenders provide you with a written disclosure of the loan's terms and conditions before you sign any paperwork.

Title loans allow you to get your hands on cash quickly, but they can cause a lot of stress if you aren't careful. The typical borrower will end up paying more in fees than they borrowed, and twenty percent of those who default on their loans will have their vehicles repossessed. Consider your financing options before settling on a car title loan to meet your financial needs.